AITA for laughing in my brother and SIL’s faces when they demanded to use my credit card?

At just 22, she stands on the brink of independence, carefully navigating the complex world of finance with cautious optimism. Living at home while finishing university, she shoulders responsibility by contributing rent and managing her own expenses, all while saving diligently for the milestones ahead—driving lessons and her first car, symbols of freedom and self-reliance.

In a deliberate step toward adulthood, she embraces the challenge of credit management, opening a credit card to build her financial foundation with wisdom and restraint. Though her credit score is modest, it reflects a promising start, a quiet testament to her determination to master the art of money before fully stepping into the vast world beyond university walls.

Subscribe to Our Newsletter

As renowned researcher Dr. Brené Brown explains, “Boundaries are the distance at which I can love you and me simultaneously.” The situation presented by the 22-year-old OP is a classic confrontation between personal financial autonomy and familial entitlement, overlaid with a power dynamic based on age and perceived vulnerability. The OP demonstrated financial responsibility by opening a credit card specifically to build credit, understanding the risks involved, and setting a low usage limit for personal financial education. The brother and SIL immediately tried to bypass this boundary, framing their request as a right or a favor owed to them for past caregiving, which is a clear tactic of emotional leverage and manipulation. The OP’s refusal was entirely appropriate; lending a credit card, especially to individuals with a history of debt from excessive use, is financially reckless and compromises the primary user's credit standing. The escalation involving the mother highlights a breakdown in recognizing the OP's adulthood and independence. The OP's primary goal—learning responsible credit management—is incompatible with allowing others with known poor habits to use the card. The resulting family conflict, while painful, confirms the necessity of the boundary. To handle this more effectively, the OP should maintain the firm refusal, perhaps communicating through their supportive father. Moving forward, the OP should limit financial discussions with the mother and brother entirely, focusing instead on strengthening their own financial footing as they prepare to transition to full-time work.

AFTER THIS STORY DROPPED, REDDIT WENT INTO MELTDOWN MODE – CHECK OUT WHAT PEOPLE SAID.:

What started as a simple post quickly turned into a wildfire of opinions, with users chiming in from all sides.

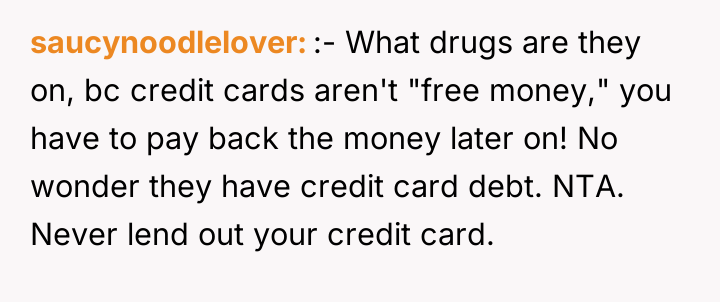

The original poster (OP) is facing a significant conflict where their decision to responsibly manage their new credit card clashes directly with the expectations of their mother, brother, and sister-in-law (SIL), who view the card as an easily accessible source of funds despite their own past debt issues. The OP strongly asserted a boundary concerning their financial tool, which resulted in escalating family tension, including manipulation attempts and temporary estrangement of the mother.

Is the OP wrong for firmly protecting their personal financial instrument and credit score from relatives who have a history of mismanaging debt, or were they overly rigid in refusing to share a resource that their family viewed as a non-issue, thereby causing severe family disruption?