Update: I cut my wife off from our finances because she wouldn’t stop ordering takeout

The original poster (OP) took severe financial action against his unemployed wife after discovering she had spent over $1,100 on food delivery services in a single month, which was unsustainable for their budget. To stop the excessive spending, the OP canceled their joint credit card and moved all available funds from the joint account into his personal account.

Immediately following this move, the wife reacted with anger, accusing the OP of financial abuse, threatening divorce, and even disposing of existing groceries to force his hand. When the wife unexpectedly stopped ordering takeout, the OP found evidence that she had taken out a high-interest, predatory payday loan to continue purchasing food, leading the OP to freeze his credit, pay off the loan in cash, and announce his intention to divorce.

Subscribe to Our Newsletter

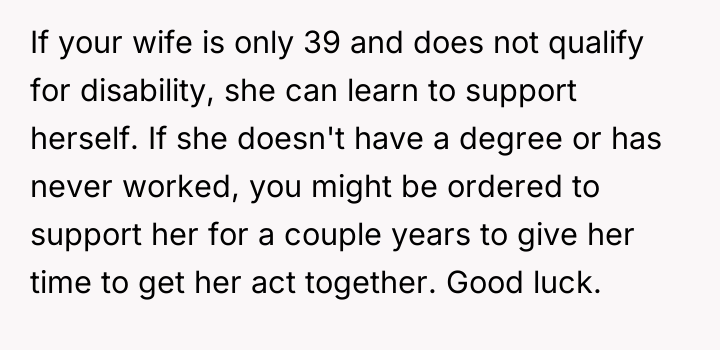

According to Dr. Finley Bennett, a specialist in relationship economics, "Financial infidelity, especially when involving predatory debt mechanisms, represents a profound breach of the foundational trust required for a functional partnership. The subsequent reaction is often proportional to the perceived violation of security." The OP's actions were a direct response to what he viewed as financial recklessness that threatened their stability. By cutting off access to funds, he attempted to enforce an immediate boundary. However, the wife's subsequent resort to a payday loan demonstrates an inability or unwillingness to adhere to that boundary through legitimate means, instead opting for a high-risk, high-cost workaround. This pattern suggests a severe misalignment regarding financial values and potentially an addiction or compulsion related to immediate gratification via food delivery. The OP was correct to protect his credit and pay off the high-interest loan, as that debt directly impacted his financial security. However, the move to divorce, while perhaps inevitable given the severity of the breach and the wife's continued behavior, should be approached with legal guidance, especially concerning alimony, as the wife is currently unemployed and has demonstrated financial instability. The path forward requires clear legal separation and possibly addressing the underlying compulsive behavior separately from the marital dissolution.

HERE’S HOW REDDIT BLEW UP AFTER HEARING THIS – PEOPLE COULDN’T BELIEVE IT.:

This one sparked a storm. The comments range from brutally honest to surprisingly supportive — and everything in between.

The core conflict centers on the wife's unchecked spending habits and her subsequent extreme actions, including taking out predatory loans, versus the OP's perceived need to enforce strict financial boundaries to protect their shared stability. The OP's decision to unilaterally seize control of the funds escalated the situation directly to the point of divorce.

The situation forces a consideration of whether the OP's immediate and drastic measures were justified as a necessary response to financial self-sabotage, or if they constituted an overreaction that destroyed the marriage by removing the wife's autonomy entirely. Readers must weigh financial responsibility against marital trust and communication.